WTF is Happening in the Economy? // Variant Perception #10

A stupid simple explanation

We’re at another one of “those” points again in history. A point where we’re getting to see the whites of the eyes of the economy. Banks are failing, savings are dwindling, real estate is freezing, and we can feel the thin fabric of reality once again.

What happens now, in these moments, sows the seeds for economic activity over the next cycle (2-5 years). So, it’s massively important to understand how we got here and what the likely paths forward hold, which I’ll cover in this newsletter and some follow-ups.

How did we get here?

The critical features of this cycle are covid, stimulus, and inflation.

COVID policies worldwide generated massive supply shocks. The supply of labor, jobs, goods, and services plummeted like never before. The global economy ground to a halt, leading to a significant "supply shock" that quickly diminished the availability of goods and services.

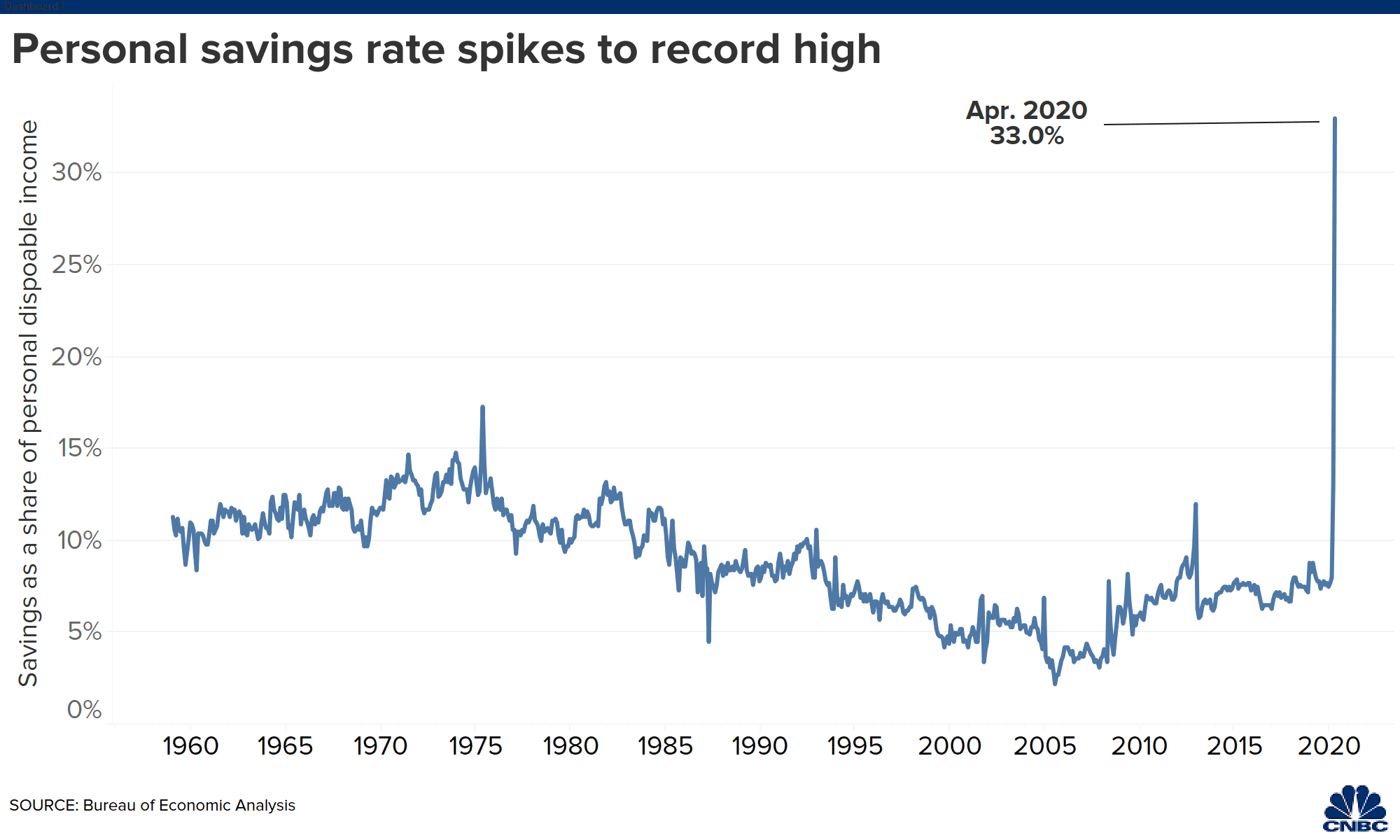

Governments intervened, supporting the economy with various programs and tools that offered temporary economic security. Rates dropped to zero (as in 2008), the Fed pledged to purchase corporate debt (a first), and most Americans received direct cash payments (PPP and stimmy checks).

This direct cash payments propelled the personal savings rate of Americans to record highs.

Then, Americans spent all that money in a closed economy, causing the largest inflation spike since the 1970s.

Remember, only two drivers of inflation exist: demand push and supply pull. Over the last two years, we experienced both. Direct transfer payments boosted demand for various goods, while the economic shutdown drastically reduced supply.

Inflation was unavoidable, but the Fed was slow to raise rates and slow the economy. Higher rates extract cash from the economy through increased debt payments, slowing growth as more money goes to unproductive interest payments.

Because the Fed lagged in combating inflation, they aggressively raised the Federal Funds rate from zero in January 2022 to 5% today – a historic increase in just one year.

The Federal Funds Rate, set by the Federal Reserve, is the interest rate banks use when borrowing money from each other short-term and serves as the basis for all interest rates charged in the economy.

Now, the pace and intensity of the rate hikes are straining sectors like banking and real estate. Any sector that relied on cheap debt after COVID and before the recent rate hikes is feeling the pressure.

Banks acquired large amounts of long-term US Treasuries at historically low yields between 2020 and 2022. When bond yields rise, bond prices fall. The rapid and substantial interest rate increases caught banks off guard with their investments.

Edward McQuarrie, a professor who examines historical investment returns, stated, "Even if you go back 250 years, you can't find a worse year than 2022," for bond holders.

Bonds are the foundation of the economy. A year deemed the "worst ever" for bond investors will have consequences, which we're currently witnessing in the banking system.

The Fed faces a dilemma: do they cut rates and ease monetary conditions to assist banks but risk fueling inflation, or do they tackle inflation and hope the fire in the banking system doesn't escalate?

We’ll find out soon what path the Fed takes. However, I believe their hand will be forced to increase debt, stimulus and spending. What we’re witnessing today is a function of long-term debt cycles, demographics, and technology.

Watch out for my next issue where I’ll dive into why the Fed’s hand will be forced.

-Jared