Let me contradict myself...

Don't sacrifice specifics in the name of convenience

Does debt cause inflation?

With our government printing record amounts of debt and our annual budget deficit shooting through the roof, I think it’s important to look at the potential effects of more debt.

Is deficit spending inherently wrong and does it mean we’re overspending?

I don’t think that’s true. Targeted deficit spending, with the proper controls (who gets the money and what the public gets in return…), can be an amazing tool for helping to support economic growth.

So, let’s see what’s happened over the last 50 years.

Our total debt as a country has exploded over the last ~70 years. But, is our nation’s debt the same as the debt that you and I might take on to buy a home? If so, we would’ve been bankrupt a while ago.

The truth is, the national debt is far different than your household debt. Because the United States issues its own currency and sets the interest rates it pays on the debt it owes, it can never go bankrupt (that doesn’t mean we can spend to infinity and not see real world consequences, however).

But, what has been the effect of all this debt? Has it caused massive inflation, runaway growth, or neither?

Since the 1970s, annual inflation rates have trended down. Our peaks are lower and have not reached over 5% since 1990 (note: I’m going to contradict myself at the end of this article about how using broad averages removes the specificity needed to make better decisions).

So, more debt is not directly inflationary. Because for the last 50 years we've added more and more debt but our inflation rate has trended down.

Now, what does all of this debt mean for our collective wealth as a nation? How does the increasing debt load affect our affluence?

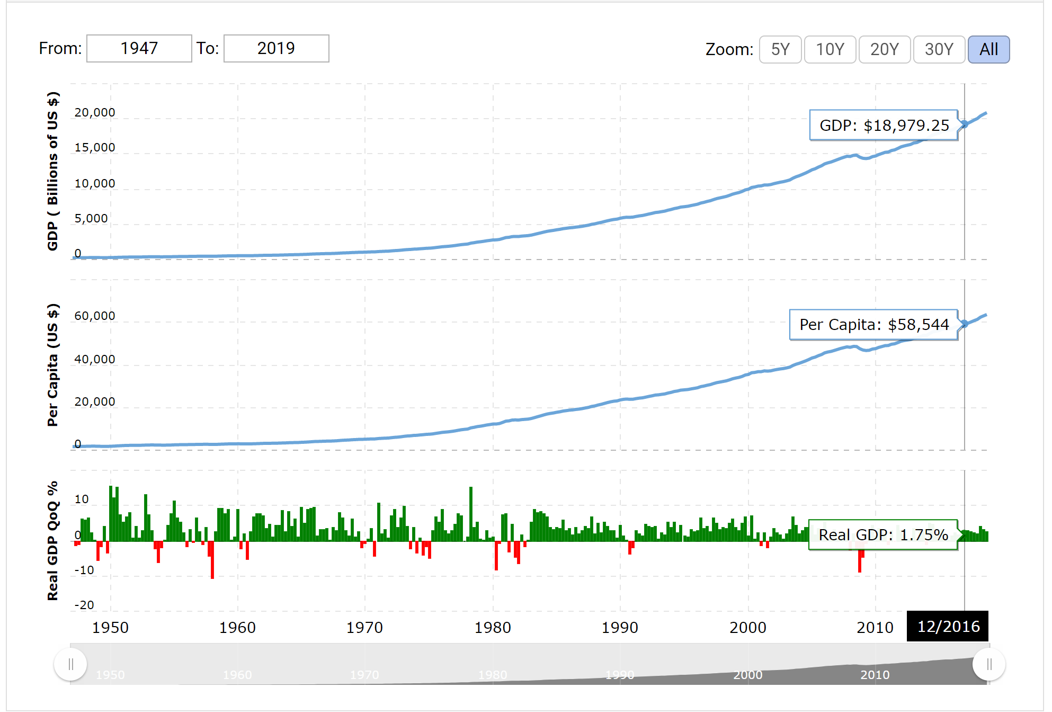

Here’s a chart of our total GDP as a country over the last ~70 years.

The line has basically gone straight up and to the right!

But, when you look at the year-over-year change, the pace of GDP growth has started to decline.

We haven’t seen higher than 5% GDP growth in a single year since the early 1980s!

So, I think it’s safe to correlate our even increasing debt load with a slower pace of economic growth.

But, let me contradict myself.

Our economy is a complex, interwoven, marketplace of millions of people. And, I find it rather ridiculous that we attempt to capture what's happening in this marketplace with aggregated and single data points.

Because when you smooth out the lines (make an average out of everything) we turn a dynamic, breathing, complex thing (our economy) into a static black and white photo.

First, I’d like to talk about two different kinds of inflation and their origins: demand-pull inflation and cost-push inflation.

Cost-push inflation is price increases caused by increased cost of production. That can be higher wages or higher prices of raw materials. Cost-push inflation is not caused by increased demand. An example of cost-push inflation would be a large wildfire that destroys the supply of lumber for the majority of the west coast. With lowered supply and constant demand, prices go up.

Demand-pull inflation is the opposite. Demand-pull inflation is a price increase caused by higher demand for a product and constant supply. This happens when there's plenty of money floating around the economy and businesses cannot expand their supply fast enough to satisfy the demand.

These kinds of inflation are not mutually exclusive. We don't necessarily get one or the other and we certainly don't only get one kind of inflation at a time.

Take my lumber example. It's true that the California wildfires destroyed large amounts of lumber supply in America. That's caused cost-push inflation. But, we're also seeing a historic housing boom which is creating more demand right at the same time as limited or reduced supply... so what's happening?

The price of lumber has increased a staggering 263% in one year!

In the United States right now, the current unemployment rate is 6%. That compares to a pandemic high of 15% and a recent low of 3.5%.

So, we can expect our government to keep spending because their math says higher unemployment means the economy can absorb this increased spending without it leading to broad inflation. But, that argument loses the specific effects to compromise for the general.

Just like my example for lumber, we're seeing the interplay of demand for scarce resources (raw materials and labor), a collapsing labor participation rate (those who are working or actively searching for work), and rising demand among specific populations.

We're seeing this with increasing prices in lithium and nickel (two main inputs for electric cars) and we're seeing a massive shortage of semiconductors. Might want to buy your Tesla or iPhone sooner rather than later!

Inflation is measured by the BLS's basket of goods. It's not specific and not comprehensive by any measure.

But in the not so distant future we will be able to track the price and velocity of sales of our entire economy, 100% anonymous, and real-time (fueled by the blockchain). This innovation will give us inflation and deflation numbers up to the second. This will allow for more direct fiscal support from the central bank and government.

We can have inflation in one area that needs to get taxed down and deflation in another that needs fiscal support. We saw this play out in 2020. Stock gains were going through the roof while business owners in hospitality and entertainment were getting whacked.

While we’re seeing increasing wealth inequality, still flat real wage growth, and politicians who grow more out of touch from reality, I am excited for the development of better data points that show the full color of our dynamic economy and allows for those that set policy to make better informed decisions.